Using BNPL to Increase Affordability Perception, Conversion, and Traffic Acquisition at HP

🧭 Context

HP sells high-value consumer electronics such as laptops, monitors, and printers across a global e-commerce ecosystem. Because these products represent a significant financial commitment, affordability perception plays a critical role in purchase completion—especially in the final stages of checkout.

At the same time, Buy Now Pay Later (BNPL) solutions were rapidly gaining adoption across e-commerce, particularly among younger audiences expecting flexible payment options.

This created an opportunity to reposition financing not just as a payment method, but as a conversion lever across the purchase journey.

🔍 Problem Framing

Initial analysis revealed that financing options were surfaced only during the payment step of checkout, when hesitation was already high due to the total purchase cost.

However, research showed that affordability is evaluated much earlier in the decision journey.

Users were asking:

“Can I afford this product?”

while browsing product pages—not when entering payment details.

At the same time:

users leaving the site to evaluate financing often did not return

cart abandonment remained high

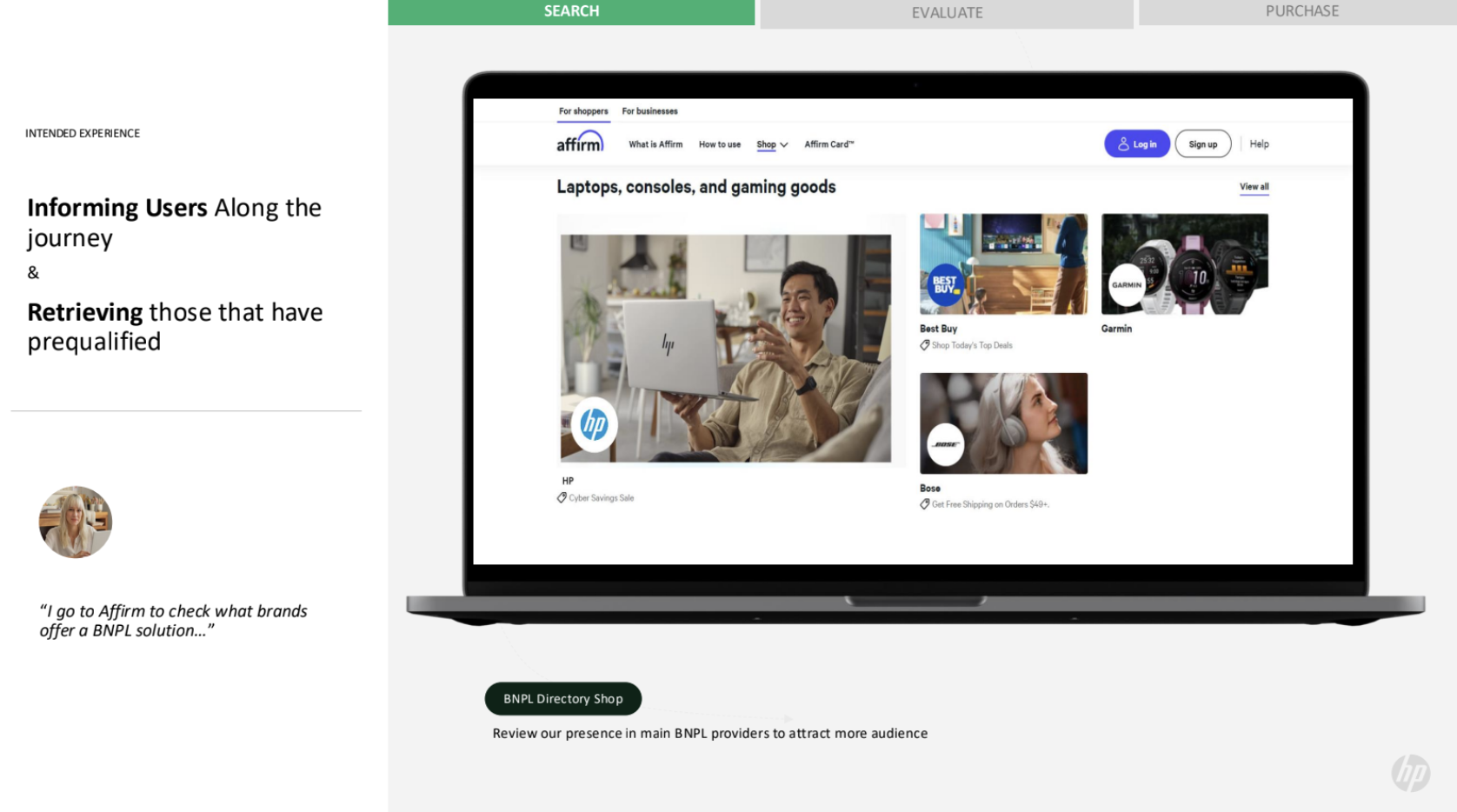

some customers started their journey directly inside BNPL ecosystems like Klarna or Affirm

This suggested that BNPL should be treated as a journey-level capability, not a checkout-only feature.

👩💼 My Role as UX Lead

I led the UX strategy for integrating BNPL across HP’s global e-commerce experience.

My responsibilities included:

defining the experience strategy for BNPL integration across the purchase journey

leading research on financing behavior in online purchasing

identifying opportunity areas beyond checkout (PDP, cart recovery, partner ecosystems)

designing cross-touchpoint integration across product page, cart, checkout, and lifecycle communication

aligning product, engineering, and business stakeholders around rollout priorities and impact expectations

This initiative required balancing conversion optimization, partner constraints, and cross-market scalability.

🎯 Strategy & Hypothesis

Instead of introducing BNPL as a checkout-only payment option, I framed it as an affordability visibility strategy across the entire journey.

The experience strategy focused on three principles:

1. Increase affordability visibility earlier in the journey

Expose monthly payment estimates directly on product pages to help users mentally reframe price perception.

2. Reduce purchase hesitation at decision moments

Provide transparent installment information before checkout commitment.

3. Extend BNPL beyond checkout into recovery and acquisition channels

Leverage financing messaging in abandoned cart emails and BNPL partner ecosystems as additional conversion drivers.

Hypothesis:

If affordability is surfaced earlier and consistently across the journey, users will experience lower hesitation and higher purchase confidence—leading to increased checkout completion.

🧠 Concept Exploration

Before defining the final experience, I explored multiple integration strategies:

checkout-only payment integration

product-page affordability messaging

cart-stage reinforcement

lifecycle-based financing reminders

BNPL ecosystem visibility as an acquisition channel

Rather than concentrating impact at a single step, I prioritized a distributed affordability strategy across key decision points.

This approach ensured that financing supported both:

conversion improvement

traffic acquisition through partner ecosystems

🧩 Experience Design Decisions

The integration was intentionally designed across multiple touchpoints to support decision-making progressively.

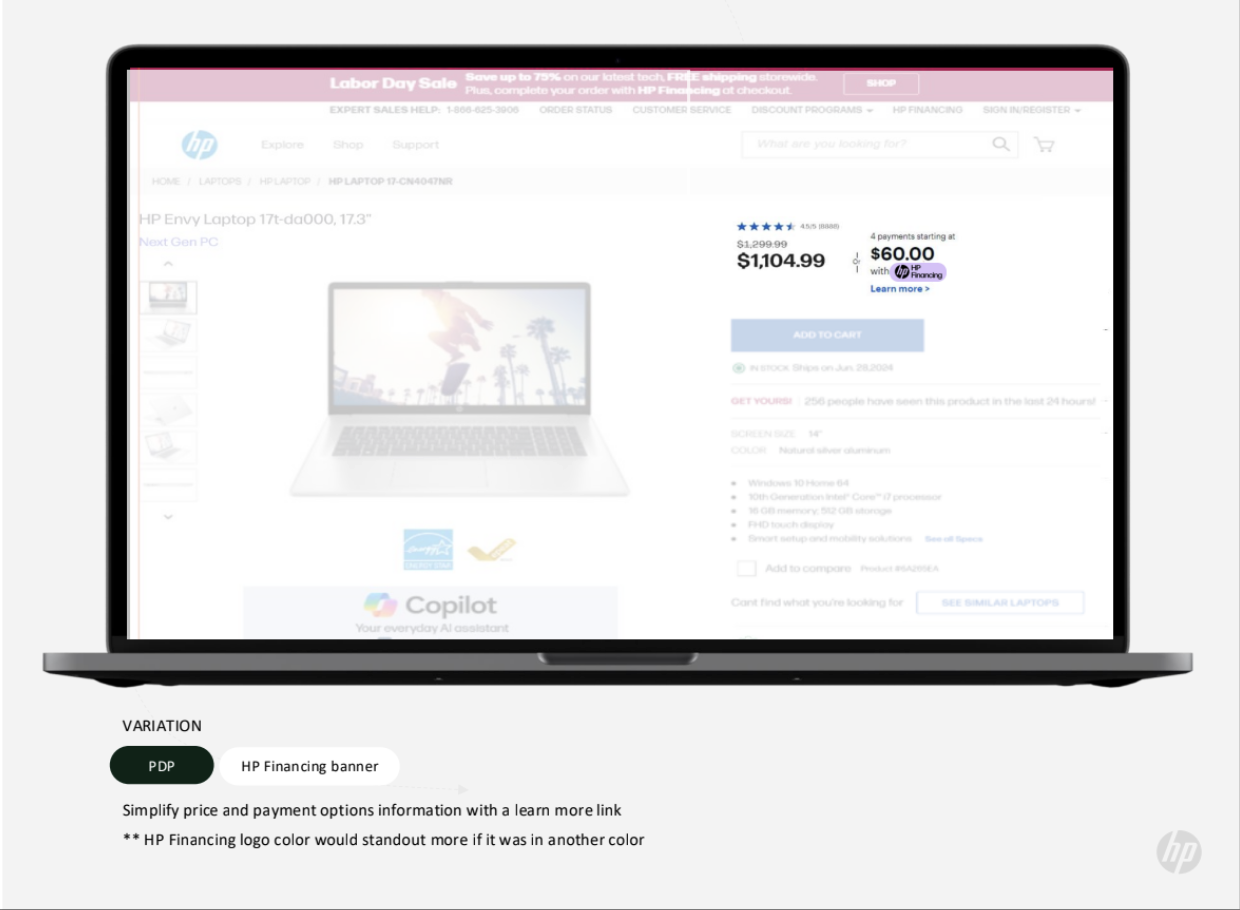

Product page

Monthly payment estimates were displayed alongside the product price to support early affordability evaluation.

Why

Users evaluate purchase feasibility during browsing—not during payment.

Outcome

Reduced early hesitation and increased confidence continuing toward checkout.